Is the Digital Rupee Your Parent’s New Superpower?

Most of us spent the last few years thinking UPI was the peak of fintech. It was fast, free, and meant we could finally leave our physical wallets at home. But in 2026, the Digital Rupee (e₹) has officially entered the chat, and it’s doing something UPI never could: it’s making money “smart.”

While UPI is just a digital bridge between bank accounts, the e₹ is actual legal tender that lives on your phone—like a ₹500 note made of code. For a student, the biggest shift isn’t just how you pay, but how you receive money.

The Rise of “Smart” Allowance

Because the Digital Rupee is programmable, it introduces a concept that will either be your best friend or your biggest annoyance: Tagged Tokens. This means the ₹2,000 your parents send for “Monthly Essentials” can now be technically restricted. If they “tag” a portion of your allowance for a specific category, the money itself knows where it’s allowed to go.

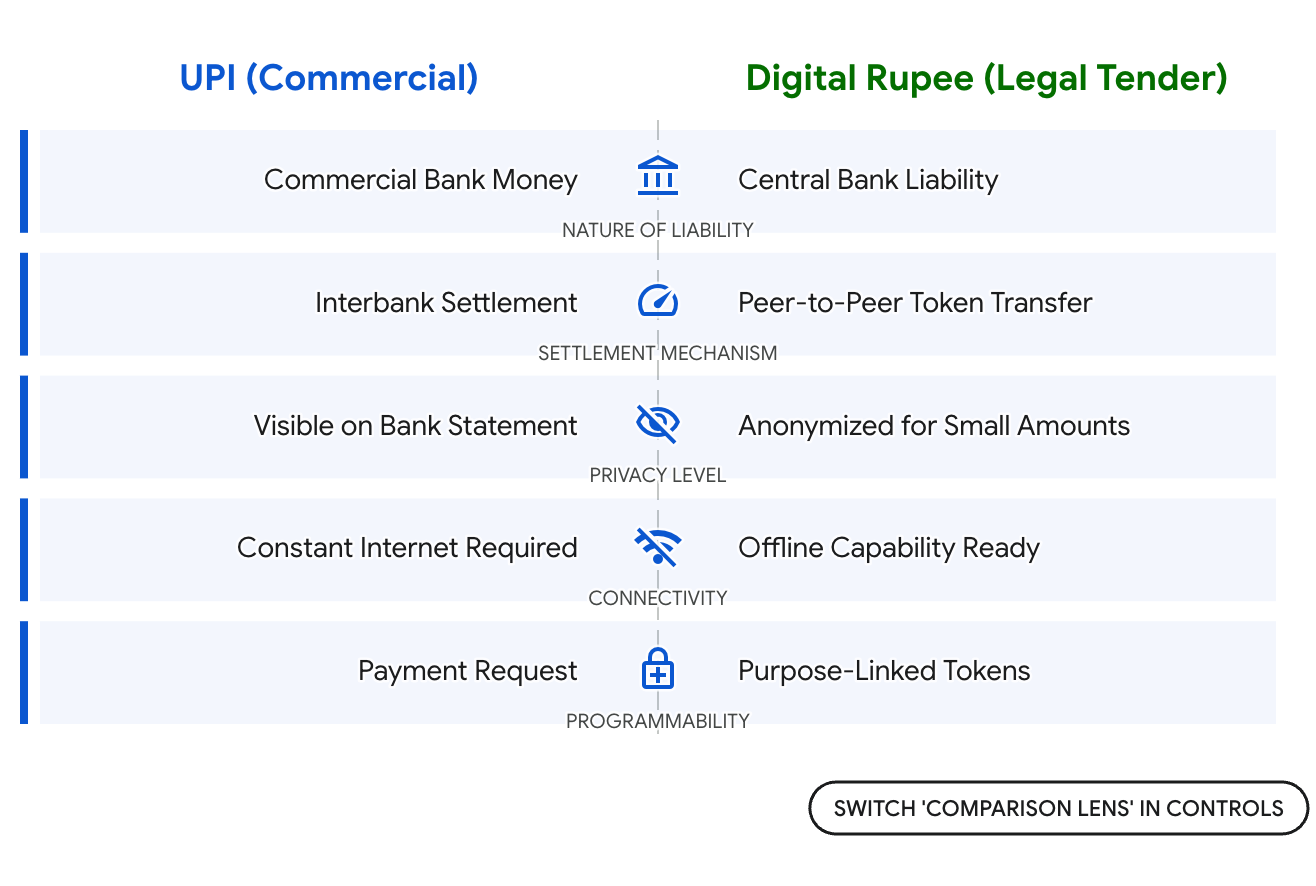

e₹ vs. UPI: The 2026 Power Shift

While both live on your phone, they are fundamentally different animals. This comparison shows how each system handles your privacy and your spending rules.

Why the “Programmable” Tag Changes Everything

The most controversial (and cool) part of the Digital Rupee is that it’s Smart Money. Because it’s a token, it can have “rules” written into it. For a teenager in 2026, this is where the “Allowance Game” gets interesting.

Parental Logic: Instead of just sending you ₹2,000 and hoping you buy that physics textbook, they can send you ₹2,000 in “Tagged Tokens.”

- The Guardrail: If ₹1,000 is tagged for Education, the transaction will only succeed at bookstores or ed-tech platforms.

- The Freedom: You get your money instantly without having to “ask” or show receipts later—the money itself is the receipt.

Check the video below to understand how this happens

This “Programmability” is why the Digital Rupee is the winner for 2026. It’s more than just a payment; it’s a tool for financial independence with built-in accountability.

Three Reasons to Switch

1. No “Server Down” Drama UPI relies on your bank’s servers being “up” at that exact second. e₹ is a peer-to-peer token transfer. It’s faster and more reliable during high-traffic lunch hours because it skips the bank-clearing middleman.

2. The Privacy Buffer Tired of your bank statement showing every ₹10 chai purchase? Small e₹ transactions are designed to be as private as cash. They don’t clutter your official bank records, keeping your daily spending habits between you and your phone.

3. Direct Perks In 2026, student scholarships and travel subsidies are being paid directly in e₹. Having your wallet ready means you get instant access to government perks without waiting days for bank processing.

Our Take : Use UPI for big, un-tagged transfers (like splitting a high-end dinner bill), but keep your “Essentials” budget in e₹. It ensures that even if you overspend your “fun money,” your bus fare and textbook funds are digitally locked and safe.

{kind=link}